Share repurchasing, commonly known as buybacks, entails a company repurchasing its own shares from the market, subsequently retiring, or holding them as treasury stock. This strategy diminishes the number of outstanding shares, thereby augmenting earnings per share (EPS) and the company's stock price, given constant or growing earnings. The efficacy of a buyback, as noted by Warren Buffett, hinges on the share price at which it is executed, buying back undervalued shares transfers wealth to shareholders, constituting a positive outcome. Equally, the converse holds true.

Source: Goldman Sachs Global Markets Weekly Wrap-up, 31 March 2024.

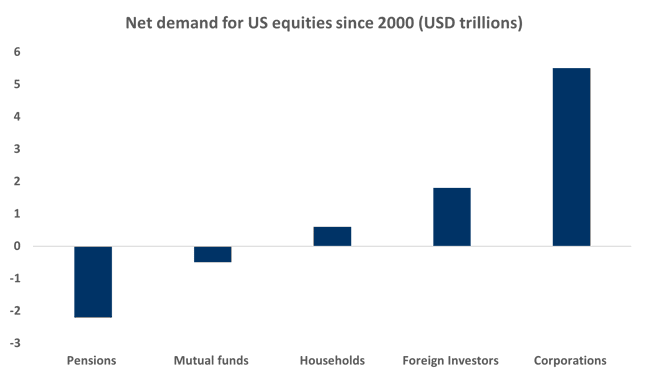

The prevalence of buyback activity started in 1982 following the implementation of SEC Rule 10b-18, which delineates the parameters of buybacks. Prior to this, while not prohibited, buybacks were infrequent due to concerns about potential accusations of price manipulation. Notably, since 2000, the primary demand for equity purchasing in the US has emanated from corporate entities.

Opinions on share buybacks are divided. Advocates assert that they offer a means for company management to redistribute surplus cash to shareholders, presenting a less enduring commitment than increasing dividends. They argue that buybacks optimise capital allocation, particularly for firms unable to achieve higher returns on investment than their cost of capital. Moreover, proponents suggest that reinvesting buyback shares into entities like venture capital/private equity fosters more growth and Research & Development investment than would occur solely through the retained earnings of large, mature firms.

Buybacks can serve as indicators, or “signals” that management perceives the shares to be undervalued, based on anticipated future growth prospects. Additionally, they may offer tax advantages for investors, as capital gains potentially are taxed at a lower rate and realised only upon sale, unlike dividends which are subject to annual taxation.

Conversely, detractors contend that buybacks adversely affect investment, employment, and income distribution. An upsurge in buybacks could signify a dearth of profitable investment opportunities for the company. Considerations of agency costs are paramount, as cash utilisation must be weighed against the expected return on all potential management decisions. Poor Management decision making, such as ill-advised acquisitions, could lead to discounted valuations of excess cash on the balance sheet. Moreover, critics argue that buybacks may serve as a tool for management to artificially inflate a flagging share price, potentially enhancing their compensation at shareholders' expense.

The discourse surrounding buybacks, both financial and political, has increased. Notably, in January 2023, US policymakers introduced a "buyback tax," levying a 1% tax on the value of any buybacks. While this tax marginally diminishes the attractiveness of share buybacks, its impact on corporate behaviour is presently considered negligible.

While historically centered in the US, the 12 months leading to December 2023 witnessed negative net equity supply in various global markets, including the UK, Japan, France, and Germany, with non-US markets experiencing the most pronounced decline. Factors such as mergers and acquisitions and heightened pressure on Japanese firms to enhance market valuations and governance have propelled a surge in buybacks, coinciding with a 33-year high in Japanese stock prices.

The erstwhile allure of buybacks was bolstered by low debt costs; however, with rising interest rates, the favourable differential between debt funding and equity costs is diminishing. Nonetheless, many companies engaging in buybacks possess significant cash reserves, rendering the cost of debt inconsequential. Should economic conditions deteriorate, certain companies may be compelled to shore up their balance sheets, reducing leverage and potentially dampening future EPS growth.

Investors must exercise due diligence and remain attentive to developments in this sphere, as certain stocks and sectors could encounter substantial headwinds should buyback activity decline.